U.S. Women’s Grooming Market Size, Share

Report Overview

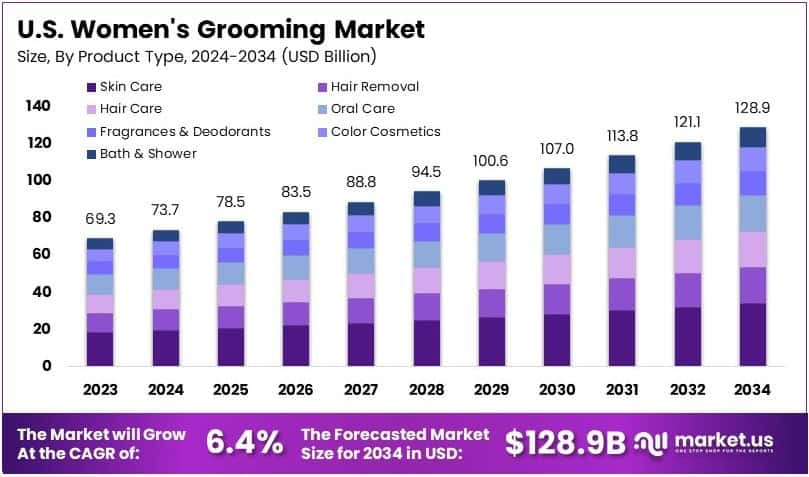

The U.S. Women’s Grooming Market size is expected to be worth around USD 128.9 Billion by 2034, from USD 69.3 Billion in 2024, growing at a CAGR of 6.4% during the forecast period from 2025 to 2034.

U.S. women’s grooming refers to personal care practices followed by women in the United States. It includes hair removal, skincare, haircare, and beauty routines. Products like razors, moisturizers, shampoos, and makeup are commonly used. These grooming habits focus on hygiene, appearance, and self-care as part of daily lifestyle.

The U.S. women’s grooming market includes all products and services used for female personal care. Market growth is driven by rising beauty awareness, changing lifestyles, and product innovation. Key players offer targeted products to meet diverse consumer preferences and needs.

The U.S. women’s grooming market is undergoing a noticeable shift, shaped by changing preferences and rising health concerns. According to the International Journal of Creative Research Thoughts (IJCRT), 67% of consumers now seek products with minimal harmful cosmetic chemicals, particularly in personal care.

This growing demand has encouraged brands to invest in cleaner formulations and promote ingredient transparency. Simultaneously, the market is seeing growth from consumers linking personal well-being to environmental health—61% now believe the environment directly impacts their health.

In particular, this shift is reflected in stronger consumer preferences for natural and eco-friendly grooming options. For instance, an Environmental Working Group (EWG) poll revealed that 75% of Americans view toxic chemicals in personal care products as a serious risk.

That number rises to 84% among women under 50. Consequently, many buyers are now turning to specialty and natural retailers for cleaner alternatives. Interestingly, 71% of household purchasers still prefer buying personal care products in-store, suggesting that product placement and retail visibility are key to brand growth.

Meanwhile, regulatory momentum is building across the country. According to EWG, 36 U.S. states introduced more than 450 bills in 2024 aimed at reducing toxic chemicals in consumer products. In contrast, the U.S. currently bans only 11 harmful ingredients in cosmetics, while the European Union prohibits 1,328. This disparity has placed increasing pressure on U.S. lawmakers to modernize regulations, especially as consumers become more informed and demand safer alternatives.

At the same time, the overall market size continues to grow. However, competition remains intense, particularly in skincare and haircare segments. As more brands adopt clean beauty messaging, differentiation becomes challenging. In response, companies are focusing on innovation, sustainability, and product simplicity to capture attention.

To illustrate, cities like San Francisco, Portland, and Austin are seeing rapid growth in natural beauty retailers, reflecting a strong local shift toward conscious consumption. On the other hand, national chains are adjusting their offerings to meet this new demand, stocking more clean-label products. This dual impact is reshaping how both small and large businesses approach inventory, marketing, and consumer engagement.

Key Takeaways

- The U.S. Women’s Grooming Market was valued at USD 69.3 billion in 2024 and is expected to reach USD 128.9 billion by 2034, with a CAGR of 6.4%.

- In 2024, Skin Care Products dominated the product type segment with 26.7%, driven by increasing consumer focus on skincare routines.

- In 2024, Supermarkets & Hypermarkets led the distribution channel segment with 35.3%, due to easy accessibility and diverse product availability.

Product Type Analysis

Skin Care Products dominate with 26.7% due to rising self-care trends, increased awareness of skin health, and demand for natural ingredients.

In the U.S. Women’s Grooming Market, skin care products lead the product type segment. Many women are now focused on personal wellness and see skincare as a part of their daily routine. Social media, beauty influencers, and dermatologists have increased awareness about different skin types and treatments.

As a result, more women are using cleansers, moisturizers, and sunscreens regularly. Brands are launching products with natural, organic, and chemical-free ingredients to attract customers who prefer safe and eco-friendly options.

Anti-aging and acne-treatment products also see high demand, especially among working professionals and teenagers. In cities like Los Angeles and New York, skincare has become both a lifestyle choice and a beauty necessity.

Hair care products are next in popularity. They include shampoos, conditioners, and hair oils that support healthy hair and scalp care. Hair removal products continue to see stable demand, especially during summer or for special occasions.

Oral care products are growing slowly, supported by a rise in whitening treatments and fresh breath products. Fragrances and deodorants remain a daily-use category, supported by seasonal and promotional sales. Color cosmetics see heavy demand during festive seasons, weddings, and social events. Bath and shower products offer comfort and relaxation, especially those with essential oils and calming scents.

Distribution Channel Analysis

Supermarkets & Hypermarkets dominate with 35.3% due to wide product range, instant availability, and strong offline shopping habits.

Supermarkets and hypermarkets lead the U.S. women’s grooming market in distribution channels. They offer everything in one place, from affordable brands to premium skincare items. Many women prefer to see, touch, or smell products before buying, which boosts in-store purchases.

Supermarkets provide deals, bundle offers, and loyalty rewards that attract regular buyers. Large chains like Walmart and Target have dedicated beauty sections, making them a top destination for grooming products. These stores are easy to access and allow customers to compare items side-by-side. In busy lifestyles, one-stop shopping at these locations is both practical and time-saving.

Online retail is growing fast with more women shopping from home. E-commerce offers convenience, wide variety, and customer reviews. Specialty stores like Ulta and Sephora cater to premium buyers who seek expert advice and new trends. Pharmacies and drugstores offer trusted brands and health-focused products, often bundled with medical care.

Convenience stores sell travel-size grooming items and quick-use products but have limited variety. The “Others” category includes salons, beauty kiosks, and subscription box services that bring curated products directly to customers. Each channel plays a role in shaping how women explore, try, and purchase grooming products across the U.S.

Key Market Segments

By Product Type

- Hair Removal Products

- Hair Care Products

- Skin Care Products

- Oral Care Products

- Fragrances & Deodorants

- Color Cosmetics

- Bath & Shower Products

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores

- Online Retail

- Pharmacies & Drugstores

- Convenience Stores

- Others

Driving Factors

Clean Beauty and Personalized Skincare Drives Market Growth

The U.S. women’s grooming market is growing steadily due to a strong shift toward clean beauty and natural skincare. More women are now choosing products with fewer chemicals and more plant-based ingredients. This change is fueled by rising awareness about skin health and ingredient safety.

At the same time, beauty brands are introducing dermatologist-recommended and clinical-grade products, which appeal to consumers who want proven results. This trend is especially popular among women dealing with skin conditions or aging concerns.

In addition, social media platforms like Instagram and TikTok play a powerful role in shaping buying decisions. Influencers often review or recommend products, which quickly attracts attention and builds trust.

Furthermore, there is growing demand for gender-inclusive and customized grooming solutions. These products cater to all skin types, tones, and preferences, making personal care feel more inclusive and targeted. As a result, brands offering tailored solutions are seeing strong engagement from younger consumers. All these factors combined are reshaping how women in the U.S. shop for grooming products.

Restraining Factors

Premium Costs and Simplified Routines Restrain Market Growth

Despite strong demand, several factors are limiting full-scale adoption of women’s grooming products in the U.S. One major challenge is the high cost of premium, clean, and organic grooming products. While interest is growing, many customers find these products too expensive for daily use.

This cost barrier prevents mass-market adoption, especially among middle-income and younger shoppers. Another challenge is the strict regulatory landscape related to skincare ingredients. Brands must meet safety and compliance rules, which slows product launches and raises development costs.

At the same time, many consumers are shifting toward minimalist beauty routines. Instead of using multiple grooming products, they now prefer simpler regimens with fewer steps. This “less is more” approach reduces repeat purchases and affects overall market volume.

Lastly, do-it-yourself (DIY) grooming tools and at-home treatments are gaining traction. Consumers are turning to at-home kits for facials, waxing, and even skincare treatments, which lowers their reliance on store-bought grooming products.

Growth Opportunities

E-Commerce and Smart Beauty Tech Provides Opportunities

The U.S. women’s grooming market is opening new opportunities through e-commerce and technology. Online shopping platforms like Amazon, Sephora, and brand-owned sites now drive a large share of sales. Subscription-based services are also growing, allowing users to receive grooming products monthly based on preferences.

This model keeps customers engaged and encourages repeat purchases. In addition, AI-driven skincare analysis is helping women choose products tailored to their skin type, age, and goals. These tools scan the skin using apps or smart mirrors and recommend customized regimens.

This tech-driven approach improves product satisfaction and builds brand loyalty. Moreover, there is rising interest in hybrid grooming products that offer multiple benefits. For example, a single product may serve as both a cleanser and moisturizer.

These multi-functional solutions save time and money, making them popular among busy consumers. Finally, sustainable packaging is becoming a major focus. Consumers now prefer grooming products that come in recyclable, refillable, or biodegradable packaging.

Emerging Trends

Zero-Waste Beauty and Digital Skincare Are Latest Trending Factor

The U.S. women’s grooming market is being shaped by powerful trends that reflect both lifestyle shifts and technology adoption. Dermatologist-endorsed skincare routines are gaining attention across social media, where beauty creators promote trusted, science-backed products.

These routines build confidence and push demand for high-performance formulas. Another strong trend is the rise of waterless and zero-waste beauty products. These items use less packaging, last longer, and align with sustainability goals.

They include solid cleansers, powder-based skincare, and concentrated serums. These formats reduce environmental impact and appeal to eco-conscious buyers. At-home laser and LED therapy devices are also trending, as women seek spa-like treatments without leaving home.

These tools help with acne, wrinkles, and skin tone, offering a new layer of self-care. Finally, there is a growing preference for vegan and plant-based ingredients. Products made with natural oils, botanical extracts, and cruelty-free processes are now in high demand.

This shift is especially strong among Gen Z and Millennials. These trends—expert skincare, sustainable formats, advanced at-home devices, and plant-based formulas—are reshaping what modern consumers expect. As they gain traction, they continue to push innovation, visibility, and sales across the U.S. grooming landscape.

Competitive Landscape

The U.S. women’s grooming market is highly competitive, with a few dominant players leading in innovation, distribution, and brand recognition. The top four companies—Procter & Gamble Co., Unilever PLC, L’Oréal USA, Inc., and Estée Lauder Companies Inc.—hold a strong position due to their wide product portfolios, strategic marketing, and strong customer loyalty.

These companies benefit from established brands that are trusted by consumers. They cover a range of grooming needs including skincare, haircare, cosmetics, and hygiene products. Their broad product lines allow them to target different consumer segments—luxury, premium, and mass-market—effectively. This variety helps them maintain market share despite changing consumer preferences.

Strong distribution networks are another advantage. These key players have a large retail presence across the U.S., both in physical stores and online platforms. They also invest heavily in digital marketing and influencer collaborations. This helps them stay relevant among younger consumers and respond quickly to new beauty trends.

Innovation is also a focus. The leading companies invest in R&D to develop new formulas and eco-friendly packaging. Sustainability and clean beauty are growing trends in the U.S. market, and these companies are adapting by offering vegan, cruelty-free, and organic products. This not only meets demand but strengthens brand image.

Acquisitions and partnerships are used to expand market presence. By acquiring niche or emerging beauty brands, these companies tap into new customer bases and introduce trend-forward products faster. This strategy helps them stay ahead in a fast-moving market.

Major Companies in the Market

- Procter & Gamble Co.

- Unilever PLC

- L’Oréal USA, Inc.

- Estée Lauder Companies Inc.

- Johnson & Johnson

- Edgewell Personal Care Company

- Revlon, Inc.

- Coty Inc.

- Kimberly-Clark Corporation

- Beiersdorf Inc.

- Church & Dwight Co., Inc.

- E.l.f. Beauty, Inc.

- SC Johnson & Son, Inc.

Recent Developments

- Skims and Skkn by Kim: On March 2025, Kim Kardashian’s shapewear brand, Skims, acquired her beauty line, Skkn by Kim from Coty. This strategic consolidation integrates beauty and skincare into Skims’ offerings, aiming to establish a unified lifestyle brand valued at over $3 billion. The first Skims-branded beauty products are anticipated to launch in 2026.

- Ulta Beauty: On March 2025, Ulta Beauty’s new CEO, Kecia Steelman, unveiled a comprehensive strategy to rejuvenate the retailer amid challenges such as store closures and declining sales projections. Key initiatives include brand building, personalization, exclusive partnerships with Beyoncé’s hair care brand Cécred, international expansion, and enhancing the retail media network.

Report Scope

link